The second of three articles on corporate valuations and capital structures.

Stock analysts say that expectations for future performance define a company’s valuation, and if the market seems disconnected from the state of the economy, it’s because investors are looking ahead. This suggests broadly shared clairvoyance among investors, something that eludes business and public policy leaders.

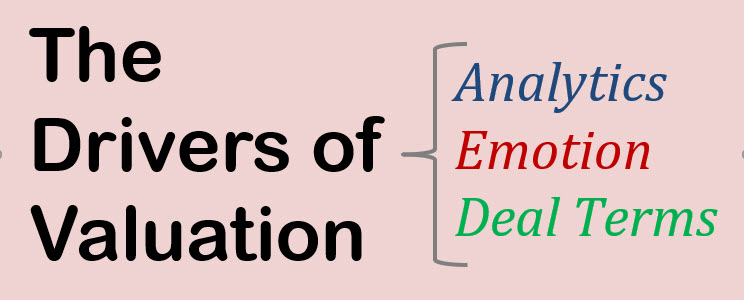

This concept equation offers another way to understand what drives a valuation. [Note: a valuation is the price to buy a company, based on the price for a fraction or share of it.]

Valuation = Analytics + Emotion + Deal Terms

It states that a valuation reflects analytics, emotion, and deal terms. These variables manifest themselves differently in the public and private capital markets.

Analytics

Investors vary in the quantity and quality of insight that informs their perspective on a stock. There are smart and not-so-smart investors in both markets but, on balance, they tend to be smarter in the private one.

A stock’s price is thought to reflect expectations for the income—dividends or capital gains— it will produce, discounted for the time value of money. Thus, the stock of a company facing difficulties might hold up if it is expected to rebound. A bad quarter will be excused if the next few should meet prior expectations. If that next quarter disappoints too, but those that follow are expected to be on track, the stock should be stable. Put another way, investors focus on what’s in the headlights, not in the rear-view mirror.

Some companies will thrive in this latest incarnation of the New Economy while others will be unaffected by the changes. For the rest, I question whether the optimism implied in the stock market makes sense, for three reasons.

1. If a company is adversely affected by the pandemic, it will take time to recover. Minimally, that means diminished projections for several quarters (i.e., lower earnings in the headlights).

2. Business models that were already in doubt are being painted with a fresh coat of it.

3. Expectations that were reasonable months ago are less so now. Assumptions about customer behavior and supply chains are less certain, for instance.

All three reasons suggest public company valuations should be lower than they are. So perhaps another one is at play—analytic thinking that anticipates investors fueled by relief and optimism as economies are reopened. A Wall Street saying captures this approach—“Buy on the rumor, sell on the news.” [A NYT article published after this one is called “Trading Sportsbooks for Brokerages, Bored Bettors Wager on Stocks.”]

Emotion

Lava lamps evoke the effect of emotion on markets. The opaque fluid—the lava—represents emotion, which rises as it is heated and falls as it cools; it’s life-like energy is beguiling. Imagine two such lamps, one with more lava than the other. The one with more is the public market, and the other is the private one. That is, while emotion affects both markets, its more evident in the public one because private investors are more valuation-aware, and they get deal terms that provide “price protection.”

Deal Terms

Deal terms are rights granted by a company to its investors. Some address governance matters—voting rights—but the ones relevant here limit valuation risk. That is, they can protect an investor from overpaying for a position.

Private investors routinely secure such deal terms. It’s hugely important for them—they would be far less successful if they had to rely on getting a valuation right when they invest. Tellingly, VCs tell entrepreneurs—“I’ll give you the valuation you want, if you give me the terms I want.”

[Guess what? NO ONE can reliably value a venture-stage company.]

A popular deal term is known as a price ratchet. It entitles an investor to additional shares at no cost if a subsequent investor gets the stock for a price that is insufficiently higher. The free shares lower the average price and increases the ownership of the protected investor.

Another deal term is a liquidation preference. It orders how the proceeds from a liquidation event—like the company being acquired—are divvied up. Think of how animals decide who eats a kill first, second, and so on—it’s the same idea. An investor with a 1X liquidation preference receives its investment back before sharing what remains with other shareholders. One with a 5X preference receives five times it’s investment before sharing.

Many deal terms are used in the private market can effectively modify a valuation.

Public investors, however, don’t get price protection. It’s ironic, given that they invest in venture-stage companies at far higher valuations. That said, an ephemeral form of price protection exists for those who get shares in a hot IPO. It’s based on investment banking practices, not deal terms. Bankers decide the price and who gets the new shares. For them, a successful IPO raises the sought-after capital at a discount of 15 to 20 percent to what the shares sell at in the secondary market. That price pop attracts investors, many of whom flip their shares. It also promotes interest in other offerings the broker-dealer has.

————————————————-

In sum, valuations work differently in the private and public markets.

In the private one, they are set infrequently by valuation-savvy investors who use analytics and emotion to assess worth but rely on deal terms to protect themselves from buying in at a price that is too high. Such an investor may wind up with a larger stake, which comes out of the position of employees and investors in a weaker position.

Public market valuations are set daily, and investors who are not valuation savvy help set them. That suggests weaker analytical ability and more emotion than found in the private market. Strikingly, public investors don’t get deal terms that mitigate valuation risk.

Why don’t public investors get deal terms that reduce valuation risk? They don’t demand them! Also, because the capital structure used for IPOs doesn’t enable special deal terms. It’s possible with a different one, however.

————————————————-

A capital structure defines ownership interests in a corporation. There are three types—a conventional one, a modified conventional structure, and the Fairshare Model. The first two are common. The third is an idea described in my 2019 book, The Fairshare Model: A Performance-Based Capital Structure for Venture-Stage Initial Public Offerings.

- A conventional capital structure has a single class of stock. In one, all shareholders are treated alike, which means no special terms. Like in Alexander Dumas’ novel The Three Musketeers, its “All for one and one for all”—all shareholders get the same deal. This type is used by public companies and private ones with non-professional investors. It’s “conventional” with respect to when a valuation for future performance is set—it happens when an equity investment is made. To illustrate, if you buy half of my new company for $1, we agree that my future performance is worth $1. Thus, the company’s pre-money valuation is $1. After you put in your money, its post-money valuation is $2. These terms are explained in this video I created years before the publication of The Fairshare Model, so the information about the book is out of date.

- A modified conventional capital structure has multiple classes of stock. Its “conventional” because a value for future performance is set when an equity investment is made. It’s “modified” because it allows a company to treat some shareholders different from others, by providing deal terms that can reset the upfront valuation. It evokes George Orwell’s Animal Farm, in which “All animals are equal, but some animals are more equal than others.” Again, VC and private equity investors require a modified conventional capital structure because one is necessary to secure deal terms they demand. Public companies occasionally have multiple classes of stock for governance reasons (i.e., super-voting shares for some shareholders), but not to reduce valuation risk.

- The Fairshare Model is unconventional. It places no value on future performance when equity capital is raised—instead it defines how to reward actual performance. It’s also novel—no company has used it yet. The Fairshare Model uses multiple classes of stock to accomplish two goals. It limits valuation risk for IPO investors. It also balances and align the interests of investors and employees—capital and labor. There are two classes of stock—both vote but only one is tradable. IPO and pre-IPO investors get the tradable stock—employees get it too, for pre-IPO performance. It’s common stock, but for simplicity, I refer to it as “Investor Stock.” Employees get the non-tradable stock for future performance—a preferred stock I call “Performance Stock.” The Performance Stock converts to Investor Stock based on milestones described in the company’s offering document, or that both classes subsequently agree on. With this structure, public investors are more likely to profit when they invest in a company with high failure risk, because they have less valuation risk. And a well-performing team can end up with more of the wealth they create than VCs would allow.

To consider the significance that reduced valuation risk can have on capital markets, perform these two thought experiments.

- Ask yourself “How might the private capital market change if VC and private equity funds could only use a conventional capital structure?” [Without deal terms to reduce valuation risk, their success would depend on having superior analytics, and not being overly swayed by emotion. I believe this would cause investing activity to dramatically shrink because private investors would be exposed to a full dose of valuation risk.]

- Now ask, “How might the public capital market change if companies used the Fairshare Model when they go public?” [Public investors would be more likely to profit when they invest in a venture-stage company, and there would be better alignment between investors and employees. As a result, venture investing would grow, and the economy be more vibrant. That’s because these types of companies are the engine of economic growth and job creation, not the Fortune 500.]

In closing, the Fairshare Model provides a framework to structure IPOs so that more average people benefit—public investors get price protection, and employees have the opportunity to earn more of the wealth they create. Thus, it can help address the epic economic challenge of the 21st Century—to distribute the benefits of capitalism more fairly and broadly.

This is the second of three related articles. The other two in the series are: